Co-author: Oygul Yuldasheva

Over the past decade, green industrialization has emerged as one of the defining economic trends of our time. The concept refers to the process by which countries restructure their industries (steel production, fertilizer manufacturing, cement production, and energy generation) to significantly reduce carbon dioxide (CO₂) emissions, while continuing to grow their economies. In practical terms, this means replacing coal- and gas-powered factories with facilities that run on renewable energy sources such as solar and wind, improving energy efficiency, and adopting production technologies that release far less carbon into the atmosphere. The underlying goal is straightforward: to ensure that economic development no longer comes at the expense of the climate.

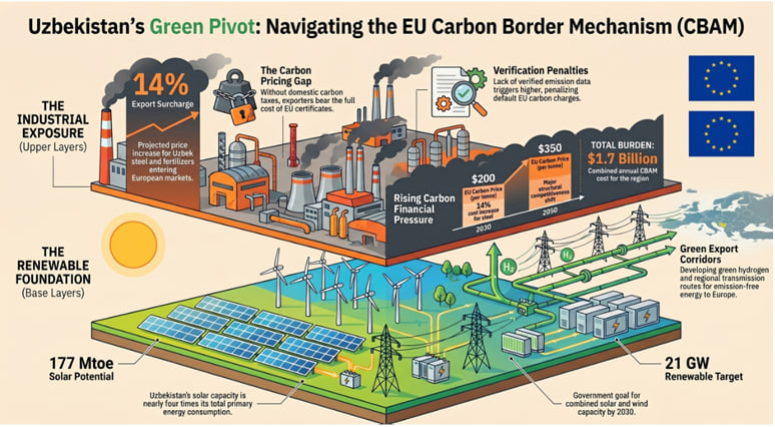

This global shift has taken on a new urgency since 1 January 2026, when the European Union fully activated the Carbon Border Adjustment Mechanism (CBAM) – a landmark trade policy instrument that directly links environmental standards to market access. Under CBAM, any company wishing to export certain carbon-intensive goods into the EU must now purchase certificates corresponding to the amount of CO₂ embedded in the production of those goods. The covered products include steel, aluminum, cement, fertilizers, hydrogen, and electricity – sectors that together account for a significant share (individually, iron and steel production contributes 7–9% of global GHG emissions, cement approximately 8%, aluminum around 2–3%, fertilizer manufacturing 2–3%, and hydrogen production close to 2-2.5%, while the power sector represents roughly 25% of global CO₂ emissions) of global industrial emissions. The rationale is to ensure that foreign producers face the same carbon cost as EU manufacturers, who are already subject to the EU’s own internal carbon pricing system.

The EU presents CBAM as a measure to prevent carbon leakage – the risk that production simply moves to countries with weaker environmental rules. Many developing economies, however, view it very differently. From their perspective, CBAM functions as a form of “carbon protectionism”: a trade barrier that uses environmental criteria to disadvantage exporters from countries that have not yet completed their own green transition. Countries that rely on fossil fuels, often due to limited financial and technological resources find their goods subject to additional costs at the EU border. This raises a legitimate concern: that CBAM may inadvertently penalize poorer nations for the same industrialization path that wealthier nations themselves followed for over a century, while simultaneously benefiting European producers who are shielded from lower-cost foreign competition.

For Uzbekistan, a fast-growing economy that exports steel, aluminum, fertilizers, and gas-related products to European markets, CBAM presents both a serious challenge and a strategic opening. On the one hand, Uzbekistan’s industrial sector remains heavily dependent on carbon-intensive energy sources, meaning its exports face higher CBAM costs and reduced competitiveness in Europe. On the other hand, Uzbekistan possesses exceptional solar and wind resources and has already launched one of the most ambitious renewable energy programs in Central Asia – a foundation that, if extended to its industrial base, could reduce CBAM exposure, attract international investment, and open doors to premium low-carbon export markets.

I. The risks of CBAM for Uzbekistan’s exports to the EU market

The EU’s CBAM applies to six product categories: cement, iron and steel, aluminum, fertilizers, electricity, and hydrogen. These are precisely the sectors in which Uzbekistan has developed export capacity and in which the country’s production remains heavily reliant on fossil fuels and aging industrial infrastructure. According to Uzbekistan’s 2024 foreign trade data, substantial volumes of exports to EU member states comprise fertilisers, ferrous metals, and aluminium, with the principal destination markets being Latvia, Lithuania, Romania, and Germany.

|

Product |

EU Importing Countries, Value (USD thousand) |

|

Fertilisers |

Latvia – 46,224 │ Romania – 22,778 │ Lithuania – 16,960 |

|

Iron and Steel |

Latvia – 4,713 │ Lithuania – 2,794 │ Germany – 523 |

|

Aluminium |

Lithuania – 10,672 │ Latvia – 968 │ Bulgaria – 115 |

According to the International Monetary Fund the total annual CBAM cost for the entire Middle East and Central Asia region will reach $1.7 billion per year – equivalent to a 14% surcharge, a kind of extra customs duty, on all goods from the region that fall under CBAM rules. Within that regional total, Uzbekistan and Kazakhstan dominate: some 90% of regional emissions covered by CBAM originate in these countries, primarily from iron and steel, aluminum, and fertilizer production. This concentration reflects the fact that both economies export large volumes of these high‑emission products, placing them squarely in CBAM’s crosshairs.

The United Nations Economic Commission for Europe (UNECE) report, provides the most specific projections for Uzbekistan. It finds that EU carbon prices are projected to rise sharply, reaching approximately $200 per ton of CO₂ by 2030 and around $350 by 2050. At those levels, the cost of Uzbek steel exported to Europe could rise by as much as 14%, fundamentally altering its price competitiveness.

The World Bank’s CBAM Exposure Index offers a nuanced picture. While Uzbek aluminum actually shows lower emission intensity than the average EU producer, potentially giving it a slight competitive advantage in that sub-sector, other key exports, particularly steel and fertilizers, face significant exposure owing to Uzbekistan’s dependence on carbon-intensive energy and dated production technologies.

A structural vulnerability compounds these direct cost pressures: Uzbekistan has not yet established a domestic carbon pricing mechanism. Under CBAM rules, exporters may deduct carbon prices already paid in their home country from their EU obligations. Without such a mechanism, Uzbek exporters cannot claim this deduction, meaning they bear the full CBAM cost – while competitors in countries with domestic carbon pricing systems may pay substantially less.

Compounding this is the verification burden. From 2026, emission reports can no longer be self-certified; they must be verified by accredited independent experts. Where data is missing or unreliable, the EU applies conservative default values that are deliberately penalizing and may overstate actual emissions. Uzbek exporters who lack robust monitoring, reporting, and verification (MRV) systems could therefore face higher effective CBAM costs than their actual emission intensity would warrant.

II. The Opportunities: Solar Energy, Modernization, and Green Certificates

The same CBAM pressure that creates risks also creates incentives and Uzbekistan has already begun to respond. The country possesses structural advantages that, if leveraged strategically, could transform CBAM from a threat into a gateway to premium green markets.

Uzbekistan’s geographic endowment is exceptional: the country enjoys among the highest levels of solar irradiation in Eurasia, with a total solar energy technical potential estimated at 177 Mtoe – nearly fourtimes the country’s entire primary energy consumption. This potential is already being activated at scale. By the end of 2025, Uzbekistan had commissioned 15 solar and 5 wind power plants with a combined capacity of 5,582 MW. Renewable assets generated 10.5 bln kWh of electricity in 2025 alone, saving 2.8bln cubic metres of natural gas and preventing 4.2 mln tonnes of harmful emissions.

The government’s 2030 target is ambitious: 54% of national electricity generation from renewables, reaching 21 GW in combined solar and wind capacity, which would save 18 bln cubic metres of natural gas annually. 2025 year was declared as the “Year of Environmental Protection and Green Economy,”and Uzbekistan has attracted approximately $35 bln in green energy investment from international partners including Saudi Arabia’s ACWA Power, France’s Voltalia and the Asian Development Bank.

The UNECE report notes that aligning power generation, hydrogen production, and industrial processes with EU-comparable carbon prices could simultaneously reduce CBAM-related costs while advancing national climate goals. The report identifies substantial opportunities for fuel switching away from coal – up to more than 600 PJ (around 167 TWh) by 2050 – alongside increased electrification, improved energy efficiency, and greater integration of renewable sources.

Already, several domestic industrial companies in Uzbekistan have adopted international green-energy certification. This certification pathway is critical: verified low-emission production provides the data foundation for calculating actual – rather than penalizing default – CBAM charges. Firms that can document clean production processes will face materially lower CBAM obligations and gain a competitive edge over less-documented rivals.

Uzbekistan has also pioneered green hydrogen production. The first industrial-scale green hydrogen facility in Central Asia commenced operations in Chirchik, powered by solar and wind energy through a public-private partnership with ACWA Power. Since hydrogen is a covered sector under CBAM, green hydrogen production positions Uzbekistan to export a commodity that, when verified as produced with renewable energy, would carry negligible embedded emissions and therefore incur minimal CBAM charges at the EU border.

Moreover, Uzbekistan, Kazakhstan, and Azerbaijan are advancing a Green Corridor initiative – a regional framework for exporting “green” electricity to Europe via undersea and overland transmission routes. The Green Corridor Alliance was formally established in Baku in July 2025, with Italy’s CESIengaged to prepare a feasibility study expected by early 2027. If realized, this corridor would allow Uzbekistan to export verified clean electricity – a CBAM-compliant, premium product – directly to European markets.

III. Recommendations for Uzbekistan's Policy-Makers and Industrial Sector

Uzbekistan should develop and implement a domestic carbon pricing mechanism – whether an emissions trading system or a carbon tax – as a matter of priority. Under CBAM rules, verified carbon costs paid domestically can be deducted from EU obligations. This single reform could significantly reduce the financial exposure of Uzbek exporters. Regional neighbor Kazakhstan have already established such systems, though at prices below EU levels. Uzbekistan could learn from these models while calibrating pricing to its economic conditions.

From 2026, the EU applies penalizing default emission values where verified data is unavailable. Uzbekistan must urgently build monitoring, reporting, and verification (MRV) capacity across its export-oriented industries. Technical assistance from the UNECE, World Bank, and Asian Development Bank (ADB) is available for this purpose. Factories with verified low-emission profiles not only reduce their CBAM liability but can use that data to market premium, “green”-certified products to European buyers who increasingly demand documented sustainability credentials.

The sectors most exposed to CBAM – iron and steel, aluminum, fertilizers – must be prioritized for energy efficiency investment and fuel switching. The UNECE report identifies fuel switching away from coal as the single highest-impact intervention, with potential savings. Public-private partnerships and concessional finance from international the EU Emissions Trading System institutions should be channeled specifically into these sectors.

Uzbekistan should explore the EU Emissions Trading System (EU-ETS) linkage or mutual recognition arrangements that would allow its domestic carbon pricing to be recognized for CBAM deduction purposes – a path pursued by Switzerland and Norway.

Uzbekistan’s pioneering green hydrogen facility in Chirchik should be scaled and replicated. The EU’s growing appetite for imported green hydrogen – driven by its REPowerEU strategy – represents a substantial long-term market opportunity for Uzbekistan, provided production is verified and transmission infrastructure is developed. The Green Corridor project, with its 2027 feasibility timeline, should be fast-tracked.

The European Union offers a range of technical assistance instruments – including short-term expert missions through TAIEX, long‑term institution‑building via the EU4Environment program, specialized training through the MED‑GEM Network, and direct engagement through the EU Delegation in Tashkent – that can be accessed to strengthen domestic monitoring, reporting, and verification systems, train operators and verifiers, and lower the compliance burden on Uzbek exporters.

If Uzbekistan consistently implements targeted and well-calibrated measures – such as introducing a national carbon pricing instrument, developing a robust MRV (Monitoring, Reporting, and Verification) infrastructure, decarbonizing energy-intensive industries, and achieving full harmonization with EU environmental standards – it will be able to transform the Carbon Border Adjustment Mechanism (CBAM) from an external risk into a strategic catalyst. Such a proactive transition would not only preserve the competitiveness of Uzbek exports in European markets but also position the country as a credible and verifiable supplier of low-carbon steel, clean electricity, and green hydrogen.

* The Institute for Advanced International Studies (IAIS) does not take institutional positions on any issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of the IAIS.